If you’re wondering, “Why did my car insurance go up?”, you’re not alone. While traffic violations and car accidents are common reasons for a rate increase, there are several other factors that can raise your premium. Insurance companies calculate rates based on risk, so any change that increases perceived risk can affect your costs.

Key Takeaways

- Driving violations, accidents, and claims can increase your insurance rate.

- External factors, like claims in your ZIP code or repair costs, may also raise rates.

- Rates usually change at policy renewal, not immediately after a minor incident.

Common Reasons Your Car Insurance Rate Increased

1. Speeding Tickets and Moving Violations

Even a single speeding ticket or other moving violation can signal higher risk to your insurer, leading to a premium increase. Serious violations, like DUIs or multiple tickets, have a larger impact. Non-moving violations, such as parking tickets, usually don’t affect your rate.

2. Accidents (At-Fault or Not-At-Fault)

At-fault accidents directly increase your risk profile. In some states, even not-at-fault accidents may cause your rate to rise based on insurer data.

3. Comprehensive Claims

Filing claims for incidents like theft, vandalism, hail damage, or hitting a deer may increase your rate, depending on your coverage and state regulations.

4. Adding Vehicles or Drivers

Purchasing a more expensive car or adding a high-risk driver, like a teen, can raise premiums.

5. Claims in Your Area

High accident or theft rates in your ZIP code may affect your rate even if your driving record is clean.

6. Moving

Changing the address where your car is garaged can increase your rate due to different risk factors in your new area.

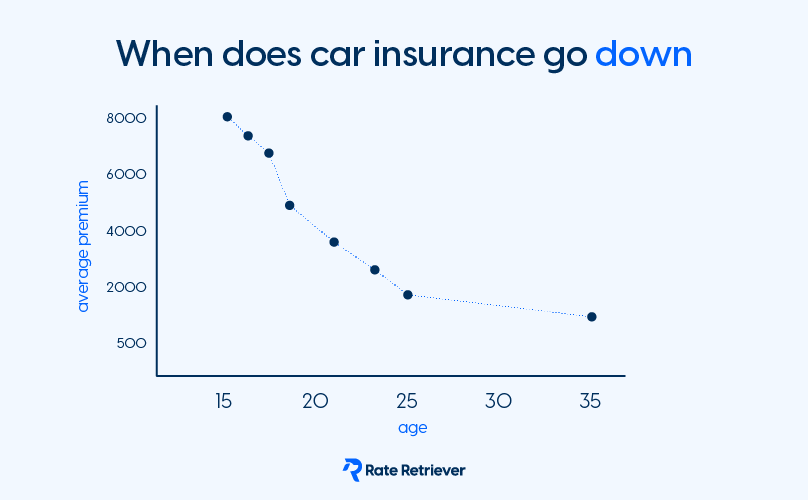

7. Age

Insurance risk changes with age. Drivers in their mid-70s and older may see higher rates, though they’re usually still lower than teen drivers.

8. Lapse in Coverage

A gap in insurance coverage can increase your rate when you start or reinstate a policy.

9. Loss of Discounts

Losing eligibility for discounts—such as safe driver, homeowner, paperless billing, or bundling discounts—can also raise your premium.

Why Car Insurance Rates Keep Rising

Rates can continue to increase over time due to rising repair and replacement costs or higher claims in your area. Personal factors, such as moving, traffic violations, or adding a driver, also contribute. Insurance companies typically adjust rates at policy renewal, so changes may not be immediate.

How to Lower Your Car Insurance Rate

- Review your coverage: Remove coverages you no longer need.

- Raise deductibles: Higher deductibles usually lower premiums.

- Compare rates: Use tools like AutoQuote Explorer® to compare against other insurers.

- Personalized savings tools: Options like Snapshot® track safe driving habits, and Name Your Price® helps fit coverage to your budget.