Getting car insurance for teens can feel overwhelming (and expensive). Since young drivers have little experience behind the wheel, insurers view them as a higher risk—which means higher premiums. But don’t worry, there are smart ways to save money while making sure your teen is properly covered.

In most cases, adding your teen to your existing auto insurance policy is more affordable than buying them a standalone policy. Many insurers—including Progressive, Geico, and State Farm—offer discounts to help families manage these costs.

Let’s break down everything you need to know about teen car insurance, from costs to discounts to practical tips for lowering your premium.

How Much Is Car Insurance for Teens?

Teen drivers are statistically more likely to drive distracted, speed, tailgate, or skip seatbelts. This risky behavior makes insurers cautious—and rates higher.

The actual cost depends on:

- Your teen’s age

- ZIP code

- Driving history (if they’ve had their license for a while)

- The car they drive

For example, a 16-year-old who just got their license will usually cost more to insure than an 18-year-old with a clean driving record. As teens gain experience, rates often go down.

👉 According to Insurance Information Institute (III), car crashes are the leading cause of death for teens, which explains why insurers charge more for this age group.

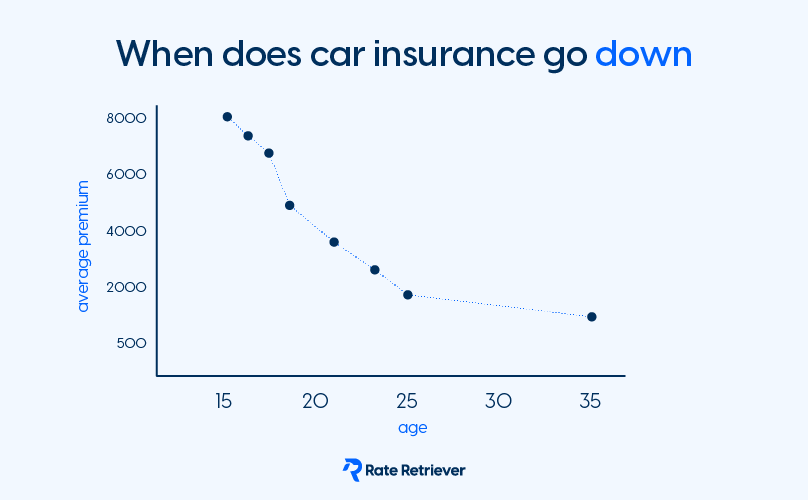

Do Rates Drop When My Teen Turns 18 or 21?

Yes! Car insurance rates generally decrease as your teen gains experience and proves to be a safer driver.

At Progressive, for example:

- Rates drop by an average of 8% at age 19

- Another 6% at age 21

If your teen avoids tickets and accidents, you’ll notice premiums slowly decrease with age.

How to Save on Car Insurance for Teens

The good news: there are plenty of discounts available to offset costs. Some of the most common include:

- Good Student Discount: Teens with a “B” average or better can often save around 5% or more.

- Multi-Car Discount: If your family has more than one car, you’ll usually get a break on premiums.

- Teen Driver Discount: Some insurers offer discounts if you’ve been insured continuously and your driver is under 18.

- Usage-Based Programs: Programs like Progressive’s Snapshot® or Allstate’s Drivewise® track driving habits and reward safe driving.

Other Ways to Save

- Raise Your Deductible: A higher deductible means a lower premium (but more out-of-pocket if there’s a claim).

- Adjust Coverage: Consider dropping extra coverage on older cars that don’t need it.

- Driver’s Ed: Completing a certified driver education program can reduce premiums. Check with your state’s requirements via your DMV.

Do I Have to Add My Teenager to My Insurance?

In almost every state, yes. Teen drivers must be insured—either under their own policy or added to yours.

Why adding them to your existing policy is usually better:

- Lower Costs: They benefit from your established driving record and discounts.

- Flexibility: If you have multiple vehicles, they’ll be insured to drive all of them.

- Convenience: You only manage one policy.

💡 Pro Tip: The only time a separate policy might make sense is if you own a luxury or sports car that you don’t want your teen driving. In that case, putting them on a cheaper vehicle’s standalone policy may save money.

How Does Coverage Work If I Add My Teen?

Once your teen is added to your policy, they share the same coverage and limits that you do. That includes:

- Liability coverage (protects you if they cause an accident)

- Roadside assistance

- Rental car reimbursement

- Loan/lease payoff

Since teens are at higher risk for accidents, you may want to increase your liability limits for better protection. Learn more about choosing the right liability coverage.

Final Thoughts: Getting Auto Insurance for Teens

Car insurance for teens doesn’t have to break the bank. By adding your young driver to your existing policy, using discounts, and teaching them safe driving habits, you can keep costs manageable.

The key is to compare rates, ask about every discount available, and make sure your coverage limits are high enough to protect your family’s financial future.

If you’re ready to explore options, you can start comparing quotes directly from top insurers like Progressive, Geico, or State Farm.